Optiva: The Goose that Laid the Golden Egg

Optiva: The Goose that Laid the Golden Egg

This article covers the entire Optiva story. It is not necessary to read my earlier posts to enjoy this article, but those posts can be found here: Optiva: The Perils of a Controlling Shareholder and Optiva: A Bizarre Situation Turns Even Stranger.

“To be simple and aligned, I’d like $50m in stock as 100% of my compensation,” reads the March 25th, 2020 e-mail from Danielle Royston, CEO of Optiva Inc., to the chair of the company’s compensation committee, Robert Stabile. At the time, Optiva’s market cap was about $112 million. “With Optiva having 5.2M shares outstanding today, [Royston] is requesting that shareholders be diluted 60% to pay the CEO for the next 4yrs of service, resulting in [Royston] owning 37% of the company,” writes Mr. Stabile in a later message to two directors on the Board. Unsurprisingly, the board rejected this demand and Royston resigned on May 11th. “The resignation followed recent compensation requests from Ms. Royston that the Board of Directors of the Company declined to meet,” reads the press release issued that day.

The details of this compensation “dispute”, along with much more from behind-the-scenes at Optiva during a tumultuous 2020, is now public thanks to a recent Ontario Securities Commission hearing. Calling the events salacious is an understatement. When first writing about the story in mid-July, analyzing Optiva from an outside perspective, I thought I had observed a few sparks and wisps of smoke. That there was something not quite right. That controlling shareholder ESW Capital might be attempting to take advantage of minority shareholders. With the OSC materials we can now step inside the company. There is no longer any doubt about what ESW was up to. The arsonist was caught in the act, but instead of retreating he became intent on taking the house down in a chaotic inferno. The behaviour that appeared suspect and subtle from the outside was actually definitive and blatant on the inside.

This is the story of an unusual attempt at minority shareholder abuse and the extreme lengths to which ESW went to first avoid losing control and then to sabotage the company. But first, let’s rewind to the beginning.

Optiva sells business support system (BSS) software used by telecom companies to measure subscriber activity on the network and bill accordingly. The company was founded in 1999, completed a couple large acquisitions in 2012 and 2015 and ran into financial trouble in late-2016 due to consistent underperformance on both revenue and profitability. ESW Capital, a secretive Texas-based investment firm controlled by billionaire Joe Liemandt and focused on enterprise software, took control of the company in early-2017 through a US$80 million rescue preferred share financing. The preferred shares gave ESW the right to nominate four of the seven members of Optiva’s Board of directors and included warrants for additional equity. Shortly after taking control of the Board, ESW fired founder and CEO Lucas Skoczkowski, replacing him with ESW-lifer Danielle Royston. Optiva then completed a C$96 million oversubscribed rights offering in September 2017 at C$31.50/share that was backstopped by ESW to fund additional restructuring. Following the rights offering, ESW owned 28% of shares outstanding or 40% on a fully diluted basis.

The rights offering through which ESW took its equity interest from 13% to 28% closed September 6, 2017. On September 11, 2017 a new ESW-owned entity was quietly incorporated in the State of Texas – ZephyrTel. At the time of incorporation, Andrew Price, CFO of ESW and one of the ESW-appointees to the Optiva Board, was listed as the sole director of ZephyrTel. According to the hearing materials, Mr. Price did not disclose his ZephyrTel directorship to Optiva. We will return to ZephyrTel in a moment.

To restructure, Optiva leveraged two ESW-controlled entities – CrossOver and DevFactory. CrossOver is essentially a remote staffing firm. Instead of having employees concentrated in expensive markets like Germany, CrossOver draws on a global network of remote contractors. DevFactory is a services provider, offering work like test writing and bug fixes. As part of the restructuring, Optiva became dependent on CrossOver and DevFactory for its operations. Optiva was now staffed almost entirely with CrossOver contractors, making it difficult to disentangle this relationship.

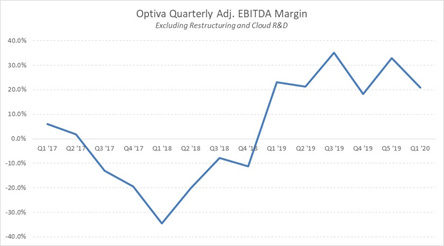

The fruits of the restructuring at Optiva materialized in improved profitability. Adjusted EBITDA margin rose from the break-even range up to 20-30% by 2019. However, revenue continued to decline apparently as customers rolled-off the platform (it can take years to switch BSS providers) and Optiva de-emphasized license and upgrade sales in the on-premise business. Shortly after joining the company, Royston pivoted Optiva’s strategy toward the public cloud, claiming telcos could reduce their BSS total cost of ownership by up to 80% using Google Cloud.

By early 2019, Optiva stock was concentrated in the hands of three large shareholders – ESW at 28%, and two Toronto-based investment funds, Maple Rock and EdgePoint, at the time holders of 18% and 13% respectively. According to the OSC materials, Royston contacted Maple Rock and EdgePoint in April 2019 seeking the blessing of the two largest outside shareholders for the sale of an Optiva subsidiary – Orga Systems, acquired in 2015 – to ESW. The stated purpose for the sale was to fund accelerated growth spending at Optiva. Uncomfortable with a potential asset sale to the controlling shareholder, Maple Rock and EdgePoint instead offered to loan the company $15 million. The offer was never accepted.

What would a sale of Orga to ESW accomplish? The suggestion from Maple Rock, relayed via the hearing materials, is that ZephyrTel lacks the key to the BSS product – a charging engine. Selling Orga to ZephyrTel could have provided ESW the cover to transfer the required Optiva IP over to ZephyrTel.

Meanwhile, ZephyrTel began executing a roll-up of software companies serving the telecom market in 2018. According to ZephyrTel CEO Mike Shinya’s LinkedIn page, accessed in September 2020, the company has to-date acquired 9 assets and is generating $70 million in annual revenue. Wouldn’t these assets have fit better with Optiva, an established telco software provider, as opposed to a brand new start-up? On April 8, 2019, ZephyrTel announced a strategic collaboration agreement with Amazon Web Services: “We expect our cloud offerings to deliver Total Cost of Ownership savings to our customers of up to 90%...” says Shinya in the press release from that day. Sounds eerily familiar, no?

It seems Maple Rock and EdgePoint grew more concerned about ESW’s influence at Optiva over the balance of 2019 and began to prepare for a confrontation. According to the hearing materials, in March 2019, Maple Rock conveyed to Farhan Thawar, one of the three non-ESW appointed directors on the Board, that Optiva should seek back-up vendors for CrossOver and DevFactory services to diminish ESW’s leverage over the company. This request apparently went unheeded.

Maple Rock also wrote to the Optiva Board in November 2019 to offer up to $50 million of fresh equity capital at a price of C$60. The proposed investment was contingent on governance improvements including engaging a compensation consultant to review pay for the CEO and hiring an independent CFO. The offer was rejected. By early 2020, through purchases in the public markets, Maple Rock’s holdings in Optiva were up to 22% of outstanding shares while EdgePoint was at 18%.

Public shareholders knew nothing of the behind-the-scenes developments – the proposed sale of Orga to ESW and the Maple Rock financing. ZephyrTel’s existence as a telco-focused ESW subsidiary was of course publicly available, though at least some in the investment community were oblivious. Well, at least I was (stage direction: the author gazes down at the floor, ashamed).

From an outside perspective, performance seemed to be improving at Optiva and 2020 looked like it might be the breakout. Revenue in the on-premise business, while still declining, was expected to flatten-out after years of focus on “customer success”. Royston stated on the November 2019 earnings call that $75 mm of revenue represented a “pretty pessimistic look” and “low watermark” compared with $100 mm of revenue over the trailing four quarters. Restructuring was almost complete and the cloud business was gaining some traction with a couple small customer wins and a positive announcement from Vodafone India.

Then, on January 20th, Optiva dropped a bombshell in the form of a very negative investor presentation. The $75 mm “pretty pessimistic” outlook for revenue was swapped out for the “melting ice cube” figure below without explanation, showing revenue falling to the $30-$40 mm range over three years. The company gave no indication of potential revenue growth from the public cloud, only noting that it may take the better part of a decade for significant cloud revenues to materialize. And management included vague plans to raise US$100 mm to invest in R&D without specifying an intended source of funds. The market cap was approximately US$200 mm at the time of the presentation.

To outsiders, this update was a shocking discontinuity in the Optiva story. But to Maple Rock, in the context of the proposed Orga sale and rejected financing offer, this was just another attempt by ESW to misappropriate value from minority shareholders. “Maple Rock believes that the recent announcement that the company is planning a USD$100 million financing is not driven by the need for additional capital, but rather is an entrenchment tactic to dilute shareholders,” declares a January 21st open letter from Maple Rock to Optiva’s Board. If Optiva truly needed additional capital, why issue a very negative investor presentation first? Why not just accept Maple Rock’s offer at $60 per share? Maple Rock requisitioned a special meeting to replace two of the three independent directors on the Board, complaining that they were not truly independent because both were former employees of ESW.

On January 29th, ESW issued a bizarre non-response to Maple Rock, “while we strenuously disagree with virtually the entire contents of your remarks, we do not believe there is value in a detailed public back-and-forth response.” The reader is left to wonder – why not? ESW then attempted to prove that they were not looking to entrench themselves by offering to sell their entire position in the company – preferreds, common, and warrants – for US$200 mm, implying a valuation of C$60 per share according to the investment firm. Remember that C$60 number, it will become important in a moment.

The ensuing months were quiet from an outside perspective. The illiquid stock, which had been stuck in the $40-$50 range for a couple years, began to fall, ultimately to about $20 per share by the end of March. Optiva scheduled the special meeting for May and then delayed it to August citing covid-related travel restrictions and an inability to host a contested AGM virtually. Odd. Then, on May 11th, Optiva announced Royston’s resignation.

This seemed highly unusual. Sudden CEO resignations are rare, Boards will go to great lengths to avoid them. But a resignation over a compensation dispute, especially in the context of ESW’s control and Royston’s ties to the firm? On May 11th, outsiders were not told the size of Royston’s ask. But $50 million of equity at a time the company’s market cap was $112 million is patently absurd. This was not a salary negotiation but a drama staged to get Royston out of the company and harm Optiva.

In e-mails to the Board, Royston claimed her request originated from conversations with Maple Rock, “As you are aware, [Xavier Majic, Maple Rock CIO] considers me underpaid…” writes Royston in her March 25th e-mail. According to the hearing materials, Maple Rock, in seeking greater alignment between Royston and Optiva shareholders, informally floated a goal for Royston to own $50 million of equity if the share price reached US$250-US$300 per share, as compared with about US$16 at the time of Royston’s request. In other words, something like 95% less than what she had asked for.

Maple Rock and EdgePoint grew increasingly concerned about ESW’s actions at Optiva and sought to eliminate ESW’s control of the Board. This process culminated in the June 26th US$90 million debenture financing, led by EdgePoint and Maple Rock, with proceeds to fund the take-out of the ESW preferred shares. Behind the scenes, negotiations around the redemption descended into chaos and it is at this point that it becomes clear ESW would not backtrack. Having been exposed, they opted to stoke the blaze into a raging inferno, trapping themselves within the flames in the process, hoping to take the company down with them.

The developments at Optiva during the month of June are tricky to follow. Instead of rehashing everything in detail, here are some highlights:

In the midst of the preferred share refinancing, ESW attempted to substitute two of its appointed directors despite the fact that, if the financing were successful, they would have been replaced in a matter of weeks.

When the initial replacement directors were rejected, ESW proposed two alternates, one of whom was Scott Royston, spouse of outgoing CEO Danielle Royston.

The hearing materials state that on June 24, 2020 discussions around a consensual preferred refinancing collapsed “due to ESW’s insistence on obtaining broad [legal] releases from Optiva and others in favour of ESW, the ESW affiliates and certain Optiva fiduciaries connected to ESW, including but not limited to Optiva’s then CEO, Royston.” On the cusp of losing control, affording outsiders the opportunity to scrub the company for the first time in years, it appears that ESW became concerned about exposure of their private behaviour to daylight.

With the preferred takeout imminent, perhaps as a last ditch attempt to avoid losing control of the company, ESW made a non-binding offer to acquire Optiva at $30 per share on Friday, June 26th. On Monday, June 29th, ESW doubled (!) its offer to $60 per share. That has to be some kind of record. All this after offering to sell their stake in the company at $60 in January.

The letter presenting the $60 offer also specifies that the proposal was contingent on completion of the debenture refinancing transaction. Meanwhile, ESW appealed to the TSX, OSC, and Ontario Superior Court of Justice to block the refinancing.

I’m not even sure how to interpret these actions charitably.

In July, with ESW no longer in control, ESW-affiliates CrossOver and DevFactory refused to accept new work orders from Optiva. The hearing materials include evidence that Jozsef Czapovics, a CrossOver contractor in the role of VP Engineering at Optiva until the end of June, tried to convince CrossOver contractors working for Optiva to leave, apparently with some success.

Separately, Optiva’s Q2 report, released on August 10th, includes surprising new disclosure about the economics of the affiliates:

“During the course of this transition, the Company has come to believe that the cost to replicate the same level of resources in-house is expected to be substantially lower than the amounts previously paid to ESW’s affiliates. Accordingly, bringing these functions in-house could result in a substantial reduction in the cost of providing the same or superior level of service on a go-forward basis. Informed by anticipated cost reductions, the Company also is reviewing the payments previously made to ESW’s affiliates.”

The related parties, far from being margin enhancers as many, including myself, had initially suspected, may have been margin detractors. Optiva spent US$146 million on services from CrossOver and DevFactory since May 2017 against a current market cap of about US$180 million. Any recovery on past amounts paid could be material for Optiva investors.

Optiva’s Q2 disclosure seems to contradict comments made by Danielle Royston on a March 2018 public call:

“Obviously, there are other vendors out there in the market that we could use to help us with this work. Certainly an outsourced dev partner, for example, would be happy to take on our bug-fix work. So we have adopted an easy framework, so everyone feels confident we are making the right decision every time we select DevFactory to provide the service. And here's the framework. DevFactory needs to be 50% cheaper than either our internal cost or an external competitive bid, or we will not use DevFactory at all. It is that simple and that clear.”

So. To summarize. ESW takes control of Optiva then starts ZephyrTel, a telco-focused software company. They acquire businesses at ZephyrTel that seem like they would have been a more logical fit for Optiva and try to sell part of Optiva’s business to ZephyrTel. They plug Optiva in to ESW-affiliates and provide assurances that the affiliates are cheaper than any alternatives. Turns out CrossOver and DevFactory were not such a great deal and ESW weaponized Optiva’s dependence on the affiliates to harm the company. Royston gave a bearish investor presentation and outlined plans for a large dilutive financing while turning down funding offers on favourable terms from the company’s two largest shareholders. Royston then resigned due to a “compensation dispute” in which she demanded 37% of Optiva’s stock. And the cherry on top - ESW bid $30 per share for Optiva on a Friday and then topped themselves with a $60 bid on the Monday, a 100% increase over a weekend.

What was ESW thinking? Did they really expect to get away with this level minority shareholder abuse? I think the answer is yes. That the extremity of the behaviour was a function of the very low odds that anyone could or would intervene to stop them. And make no mistake, the odds were very low. ESW came very close to getting away with this. Why worry about how your behaviour will look when exposed to the light of day if the odds of that ever happening are vanishingly small?

Consider that: ESW controlled the Board, with six of the seven directors having ties to ESW. The CEO was ESW-affiliated. There was no independent CFO at the company for much of the time it was under ESW control. Virtually all work at the company was being done by CrossOver and DevFactory, ESW affiliated-entities from which it would be difficult to disentangle. ESW owned 28% of outstanding shares with warrants to go to 40%. Of the roughly 32% of shares outstanding that are not held by Maple Rock, EdgePoint, or ESW, at least 9% (or 28% of the 32%) are held by parties that may have sympathies to ESW – Royston plus two Texas-based investors, Kleinheinz Capital Partners and LKCM Investment Partnership.

Consider everything that Maple Rock and EdgePoint had to do to wrest control from ESW. Active engagement with Optiva over a couple years. Significant legal battles. ESW could be forgiven for assuming that most shareholders would choose to cut and run rather than engage in such an intense struggle for control. But for the actions of Maple Rock and EdgePoint, ESW almost certainly would have succeeded at transferring very significant value to themselves at the expense of minority shareholders.

Seen through this lens, ESW could be forgiven for feeling secure in the assumption that they could behave with abandon. The odds of today’s outcome transpiring were vanishingly low. Once this outcome became a possibility and then a probability, ESW became afraid. They resorted to every possible tactic to prevent their loss of control and the associated exposure of their misdeeds. By the slimmest of margins they were caught.

And where to from here for Optiva and its shareholders? ESW’s bid for Optiva at $60 always looked unlikely to succeed with Maple Rock and EdgePoint in control of the majority of the non-ESW held shares outstanding at the company. With the OSC’s ruling on September 14th, the bid is dead. I don’t see a realistic path forward for ESW to regain control of Optiva in the near-term, absent a bid at a price that would be acceptable to Maple Rock or EdgePoint. This would have to be at a price well in excess of $60.

On a fully-diluted basis, ESW does own almost 40% of the outstanding shares with another at least 7-8% of diluted shares in friendly hands, leaving them very close to the 50% required voting threshold. As part of the original 2017 preferred share financing, ESW is required to abstain from voting their common shares in respect of director nominations. My understanding is that this requirement remains in-place indefinitely, seemingly leaving Maple Rock and EdgePoint securely in the driver’s seat. But there is risk if that requirement lapses in the future or ESW can figure out a workaround.

It feels somewhat pointless to opine on the attractiveness of Optiva stock at current levels. Already illiquid, Optiva shares have effectively ceased trading. Fair value is a function of the true outlook for revenue in the on-premise business (not that provided in the negative January presentation), the outlook for cloud, the (higher) margin profile without the related party agreements, any value destruction during the control transition, and any potential legal recoveries from ESW. All of these are quite uncertain. Trading at about 3x revenue, I am biased positively.

There is one small piece of the Optiva puzzle that remains a mystery to me. After resigning from the company, Royston couriered a copy of the children’s book, “The Goose that Laid the Golden Egg,” to representatives of Maple Rock and EdgePoint. The moral of the book is that those who have plenty want more, and so lose all they have. On whose behaviour was Royston passing judgement? Maple Rock and EdgePoint? Really? Does insisting on basic minority shareholder protections constitute excessive greed? Her own compensation negotiation? Perhaps. Or was it an act of contrition? A subtle wink to Maple Rock and EdgePoint that, through all the fighting, she harboured secret sympathies for their position. That she knew ESW had gone too far at Optiva and in so doing had risked too much, not just the prospects for its Optiva investment, but its reputation. There was always a path to 100% ownership at Optiva. All they had to do was pay a fair price.

Who or what is ESW really? It would probably be most appropriate to characterize it as a family office under the direction of Texas billionaire Joe Liemandt. He is the man behind the curtain, out of public view, not directly partaking in any of the action at Optiva. And yet, he may be the person most responsible. From the affidavit of Robert Stabile, director of Optiva: “While Liemandt had no official role at Optiva, based on my interactions with [Royston], as CEO of Optiva, [she] acted as if she reported to and took instructions from Liemandt.” I wonder if Royston sent a third copy of “The Goose that Laid the Golden Egg” to Liemandt?

Disclosure: the author owns shares in Optiva.