Optiva: The Perils of a Controlling Shareholder

Optiva: The Perils of a Controlling Shareholder

On January 21st of this year, Maple Rock Capital Partners released an open letter to the Optiva Board. “Maple Rock is very concerned that the company has issued an analyst presentation with the apparent goal of making the company look weaker than it is,” begins the section of the letter entitled “Financially Questionable Information Provided to the Market”. I’ve been closely following the markets for over a decade now. I’ve seen many cases of excessively optimistic outlooks from management. But I can’t say I’ve ever seen a management team deliberately provide an investor outlook that is worse than reality.

Was Maple Rock correct that yes, in fact, the Optiva management and Board were trying to misrepresent the situation at the company? Why would they do that? And what does this say about the potential of Optiva shares? Before answering these questions, we must take a detour through history.

Optiva (previously Redknee Solutions) sells business support system (BSS) software used by telecom companies to measure subscriber activity on the network and bill accordingly. The software is mission-critical; without it, the communication service providers cannot generate revenue. The company was founded in 1999 and completed the transformational acquisition of Nokia’s BSS operations in late-2012 followed by the purchase of Orga Systems out of bankruptcy in 2015. Management had promised that synergies from these acquisitions would drive EBITDA margins to the 20-25% range, but results never came close reaching only 14% in 2015 and otherwise hovering around break-even. Revenue also collapsed, falling from US$258 mm in 2014 to US$138 mm in 2017.

The poor results at Redknee came to a head in late-2016 as the company sought additional capital to fund ongoing restructuring and repay US$50 mm of bank debt. Redknee first announced an agreement with Constellation Software under which Constellation would: (i) purchase US$80 mm of 10-year 10% preferred shares, (ii) have the right to appoint the majority of directors, and (iii) receive 10-year warrants for roughly half of Redknee’s common equity with a C$60 strike (split-adjusted). ESW Capital, a secretive Texas-based private equity firm controlled by billionaire Joe Liemandt and focused on enterprise software, owned 11.5% of Redknee common shares at the time. ESW beat Constellation’s financing proposal by cutting the quantity of warrants in half.

ESW took control of the Board in early-’17 and quickly determined the situation was worse-than-expected. The Board fired founder and CEO Lucas Skoczkowski, replacing him with Danielle Royston from ESW and determined additional restructuring was required. Redknee completed a C$68 mm oversubscribed rights offering in mid-2017 at C$31.50/share that was backstopped by ESW. Following the rights offering, ESW owned 28% of shares outstanding or 40% on a fully diluted basis.

To restructure, Optiva leveraged two ESW controlled entities – CrossOver and DevFactory. CrossOver is essentially a remote staffing firm. Instead of having employees concentrated in expensive markets like Germany, CrossOver draws on a global network of remote contractors to populate Optiva’s workforce. DevFactory is a services provider, offering work like test writing and bug fixes. As part of the restructuring, Optiva became dependent on CrossOver and DevFactory for its operations. It would be difficult to disentangle these relationships because Optiva is now staffed mainly by CrossOver contractors.

I took a position in Optiva in the lead-up to the rights offering. While there was a lot of mystery surrounding ESW, they had been active with one other public company, Upland Software, which saw EBITDA margins expand from zero to 30-35% once ESW became involved. CEO Danielle Royston seemed highly knowledgeable on the public conference calls, the software appeared to be very sticky, and Constellation’s interest also served as validation from a highly intelligent software investor.

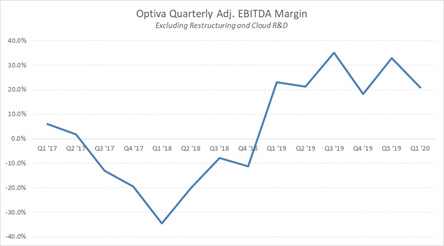

The fruits of the restructuring have materialized in the margin performance over the past couple years with adjusted EBITDA margins moving from break-even or negative to the 20-30% range. However, revenue has continued to decline as customers roll-off the platform (it can take years to switch BSS providers) and Optiva has de-emphasized license and upgrade sales in the on-premise business. Shortly after joining the company, CEO Danielle Royston pivoted Optiva’s strategy toward the public cloud, claiming the Optiva offering on Google Cloud could reduce the total cost of ownership by up to 80%.

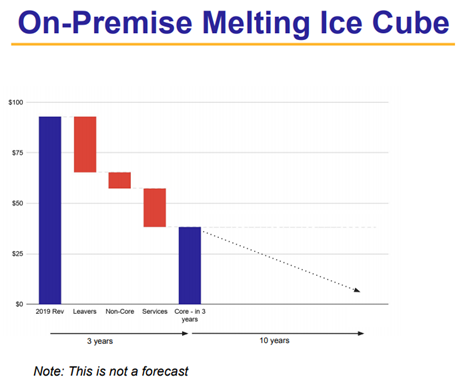

Heading into the year, 2020 looked like it might be the breakout for Optiva. Revenue in the on-premise business, while still declining, was expected to flatten-out after years of focus on “customer success”. The CEO stated on the November 2019 earnings call that $75 mm of revenue represented a “pretty pessimistic look” and “low watermark” compared with $100 mm of revenue over the trailing four quarters. Restructuring was almost complete and the cloud business was gaining some traction with a couple small customer wins and a positive announcement from Vodafone India.

On January 20th, Optiva dropped a bombshell in the form of a very negative investor presentation. The $75 mm “pretty pessimistic” outlook for revenue was swapped out for the “melting ice cube” figure below without explanation, showing revenue falling to the $30-$40 mm range over three years. The company gave no indication of potential revenue growth from the public cloud, only noting that it may take the better part of a decade for significant cloud revenues to materialize. And management included vague plans to raise US$100 mm to invest in R&D without specifying an intended source of proceeds. The market cap was approximately US$200 mm at the time of the presentation.

In the days following, Maple Rock, holders of 22% of Optiva shares, called for governance improvements in response to what they viewed as entrenchment tactics by ESW. In other words, ESW was trying to make Optiva look worse so that they might take additional control on-the-cheap. Maple Rock revealed that they had offered to invest capital twice – in the form of a C$15 mm loan and a C$50 mm equity investment at C$60 per share – and were rejected. The preferred shares gave ESW the right to elect four of the seven members of the Board, but two of the directors designated as independent were also affiliated with ESW. Maple Rock called for a special meeting to replace those two directors.

On January 29th, ESW issued a bizarre non-response to Maple Rock, “while we strenuously disagree with virtually the entire contents of your remarks, we do not believe there is value in a detailed public back-and-forth response.” If Maple Rock’s concerns were so off-base, why not provide at least a brief rebuttal? ESW then attempted to prove that they were not looking to entrench themselves by offering to sell their entire position in the company – preferreds, common, and warrants - for US$200 mm, implying a valuation of C$60 per share according to the private equity firm. The illiquid stock, which had been stuck in the $40-$50 range for a couple years, began to fall on the back of these developments, ultimately to about $20 per share by the end of March.

Things went quiet for a couple months. Optiva scheduled the special meeting for May and then delayed it to August citing covid-related travel restrictions and an inability to host a contested AGM virtually. Really? Then, on May 11th, Optiva announced the resignation of ESW-affiliated CEO Danielle Royston following “recent compensation requests…that the Board of Directors of the Company declined to meet.” Again, really? A press-released CEO resignation over a compensation dispute? Add that to the list of things I’d never seen prior to Optiva.

Hang in there, this last bit is confusing. On June 26th, Optiva announced a US$90 mm debenture financing from EdgePoint (18% shareholder) and Maple Rock (22% shareholder) with proceeds to fund the redemption of the ESW preferred shares. This financing would eliminate ESW’s control of the company. In the process of negotiating for the pref redemption, ESW took some unusual actions. The Texas-based firm had sought to replace two of its appointees on the Optiva Board with nominees affiliated with ZephyrTel, an ESW-owned cloud software provider to Telcos founded in 2018. The nominees were rejected because the independent Optiva directors determined the two companies are potential competitors (ZephyrTel appears to offer a range of cloud-hosted software solutions to telcos, including BSS).

Why would ESW do that? With the preferred takeout imminent, the new directors would have been replaced within weeks anyways. In response to the rejection, ESW requested an immediate renegotiation of the related-party agreements with CrossOver and DevFactory and stated that ESW would need to “dramatically reduce its involvement with Optiva or entirely acquire Optiva”. ESW made a preliminary, non-binding offer to acquire all Optiva shares for which no price was disclosed.

Following the announcement of the debenture financing, Optiva removed ESW-affiliated CEO Danielle Royston about a month before her scheduled exit date. In a July 6th regulatory filing we learned that, in the course of negotiating for redemption of the preferred shares, ESW sought “broad releases” from Optiva for ESW’s nominees on the Board and CEO Danielle Royston. The legal releases were not provided.

Whew – are you still with me?

So is Maple Rock correct that ESW tried to make Optiva look weaker than it really is? In my opinion - yes. In a normal situation, a firm looking to raise capital would err on the side of over-optimism, not pessimism. Instead, the CEO slashed her revenue outlook for the core business in half from a “pessimistic” view provided only a couple months earlier. The company also provided zero indication of the revenue opportunity from the cloud, despite the fact that it is the sole strategic focus of the firm and some customers are already live on the platform. Disclosing plans to raise US$100 mm with no source of proceeds was also highly unusual.

I suspect that ESW thought they could “pull one over” on the public shareholders and increase their control of the company at a cheap valuation. The January presentation even alluded to the potential for a portion of the US$100 mm funding to be used to redeem some of the preferred shares. This would have been a great outcome for ESW – maintain control of the Board by leaving a small amount of prefs outstanding (say US$20 mm), but effectively roll the remaining US$60 mm of prefs into common equity with more upside potential.

I am speculating a bit here, but I wonder if ESW was looking to tighten its grip on Optiva so that it might more closely integrate operations with ZephyrTel. As a critical vendor to over 100 telcos, Optiva has customer relationships that could be leveraged to sell ZephyrTel products. ESW’s actions in recent months suggest to me that they are worried about legal repercussions from their activities at ZephyrTel while in control of Optiva. Nominating replacement directors for the Optiva Board mere weeks before the directors would be removed anyways due to the refinancing makes no sense. I wonder if ESW did this in the hope that Optiva would have allowed the substitution and thus tacitly acknowledged that there is no conflict with ZephyrTel. Legal releases sought during the negotiations over the preferred shares clearly had a similar intent. Last, reading the tea leaves, it appears possible to me that Danielle Royston is headed to ZephyrTel. If this in fact proves to be the case, the optics are quite difficult. Resigning from Optiva due to a compensation dispute with the ESW-controlled Board only to move to a competitor fully-owned by ESW?

I can only assume that ESW has been surprised by the way things have played out. They have now lost control of Optiva while I believe their desire was actually to tighten their grip. It was only the presence and actions of Maple Rock and EdgePoint that narrowly thwarted their efforts and protected minority shareholders from what may have been a very dilutive financing.

There remain many question marks for investors in Optiva. Has any damage been done to the operational or strategic positioning of the business as a result of having a misaligned CEO and Board? What are the implications for the margin structure and ability to execute on the cloud opportunity if Optiva is forced to disentangle from CrossOver and DevFactory? It appears likely that the January outlook offered by management was overly negative. What would a more realistic appraisal look like?

Assuming on-premise revenue stabilizes at US$75 mm, Optiva is trading for about 2.5x revenue or about 10x EBITDA with margins of 25%. This seems like a roughly fair valuation for a no-growth software company. But Optiva has a leading position in public cloud. While the timing on the transition to the cloud is uncertain, the direction of travel seems clear. Moving to the cloud should drive revenue 2-3x higher per customer and make it less lumpy. There is also a share gain opportunity with new customers. In a good case scenario, we could see revenue at multiples of the current level within five years.

Developments at Optiva this year make for one of the more bizarre business stories I have seen in my career. The lesson, if there is one, might be this - be cautious of controlling shareholders, even when they appear aligned.

Disclosure: the author owns shares in Optiva.