Mystery at High Arctic

Mystery at High Arctic

Failing to Understand an Unusual Corporate Reorganization

The High Arctic Board of Directors has some explaining to do.

High Arctic is a microcap energy services company with operations in Papua New Guinea and Canada. In July 2022, the company sold the bulk of its Canadian business to Precision Drilling for $38 million leaving it with the PNG business, cash, and some smaller assets in Canada. The press release announcing the sale of High Arctic’s Canadian business quoted long-time Chairman Michael Binnion:

“After reflection on High Arctic’s core strength and future opportunities, the Board made a strategic decision to divest certain assets in Canada and focus on resurgent opportunities associated with our existing business in Papua New Guinea. PNG is a market where we have a dominant position, a history of high profit margins and free cash flow generation, and where the Corporation’s future fortunes are inextricably tied.”

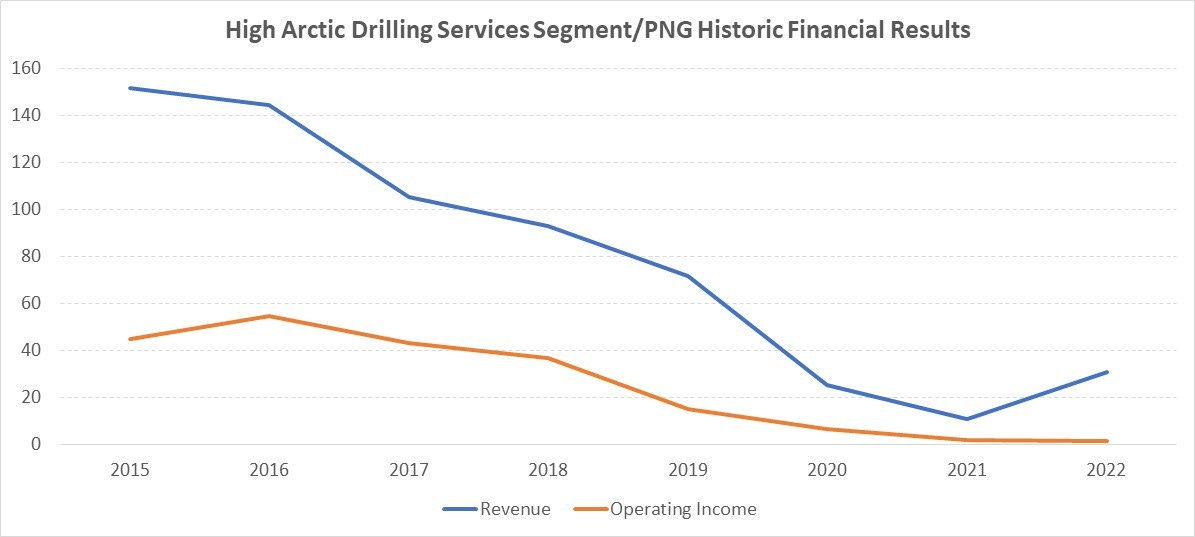

PNG is a resource-rich country, but a difficult one in which to operate. PNG’s terrain is mountainous and tropical while its population is poor and rural. High Arctic provides drilling services in PNG and owns two heli-portable rigs. The terrain and lack of road access mean rigs sometimes need to be moved to drill sites via helicopter. High Arctic’s PNG business generated significant revenue and operating income at the peak of the prior cycle in 2016, delivering $55 million of operating income. The current market cap of the company is less than $60 million with $47 million of cash on the balance sheet.

PNG results were soft in recent years because of covid and weaker conditions in the energy market. High Arctic’s heli-portable rigs have largely been idle, though the company does earn decent revenue as a service provider on third-party equipment. However, as noted by the Chairman in the 2022 press release, there are “resurgent opportunities” in PNG. Specifically, the imminent construction of a liquid natural gas export terminal by TotalEnergies and Exxon, scheduled for a final investment decision in 2024.

Selling lower-quality, non-core assets to focus on the business in PNG just ahead of a potential inflection in market conditions – so far so good.

In May 2023, the company surprised investors, announcing a spinoff of its PNG business to shareholders and the distribution of the bulk of the cash on its balance sheet. But there was one catch. The PNG business would be spun off as a private company, a highly unusual action for a public company to take. CEO Mike Maguire stated in the May 11th press release:

“I am excited that the Board intends to reorganize the Corporation, starting with a tax efficient return of cash to shareholders. The proposed spin-off of the Papua New Guinean business will allow senior management to concentrate where we have had the most success in the past…Our PNG business has been consistently undervalued by the public market, and we believe that the current market conditions make it appropriate to take steps to unlock value. I believe our customers and employees in both PNG and Canada will appreciate and benefit from a locally managed business.”

Public companies spinoff businesses all the time. But a private spinoff from a public company? Investors on the earnings call were puzzled:

Investor: “I’m not a sophisticated investor, but if I end up with shares in a private company based in Papua New Guinea, how do I get rid of them if I don’t want them?”

CEO Mike Maguire: “Yes, it’s a very straightforward question you’ve asked there. And at the moment, I cannot give you a direct answer to that question. If there is a buyer and there is a seller, a transaction can be made. As far as an intermediary to potentially facilitate such transaction, that is something I’m not able to answer at this time.”

And the following quarter:

Investor: “Mike, walk me through this transaction. I know it hasn’t been finalized yet. But right now, I own as a shareholder, I own each of the pieces, one being $0.75 worth of cash, one being the operations in PNG and the other one being whatever is left in the public company…”

CEO Mike Maguire: “So the way in which the transaction is structured is that you would receive the $0.75 of cash, a right to buy a share, an equivalent share in High Arctic’s PNG business, and you would retain your share that you hold in the Canadian business. The sale of PNG would then return the proceeds back into the Canadian business, which you would still own your share of.”

Investor: “There was also a comment on the right being traded. Virtually every transaction I’ve ever worked with, the exchange does allow that. So I’m not sure why they wouldn’t allow you to list the rights in this case…”

CEO Mike Maguire: “We would love to be able to do that. As I understand it, as explained to me by the lawyers who are smart enough to properly understand it, because the right is to buy a private company, and it may have something to do with it being foreign as well...it can’t be listed”

So public shareholders will receive a right to buy a piece of the private PNG business. Given the rights will not be publicly tradeable nor would shares in the newly private company, some shareholders would not exercise their rights. This would permit investors that do wish to participate in the newly private PNG business to acquire their stake at a discount.

Enter Cyrus Capital Partners, a New York-based investment firm and High Arctic’s largest shareholder at 45%. Cyrus acquired its stake in High Arctic more than 10 years ago as part of a balance sheet restructuring and had two representatives on the Board at the time the proposed reorganization was announced. It is almost inconceivable that the Board would forge ahead on a path that would be doomed to fail without the support of its largest shareholder if that shareholder did not support the plan. It is also not difficult to imagine why Cyrus might be in favour of such a reorganization, providing it with the opportunity to acquire shares in the soon-to-inflect PNG operations cheaply from shareholders that can’t or won’t invest in a private entity. VN Capital, a 5.6% shareholder, expressed exactly this concern in an August open letter to the Board1.

Interestingly, one of the Cyrus representatives, Ember W.M. Schmitt, did not stand for re-election in 2023 and so left the Board at the AGM which occurred immediately after the reorganization was announced. The other representative, Dan Bordessa, Vice Chairman at Cyrus, resigned from the Board in early August, a few weeks before VN Capital published its open letter. Bordessa is not quoted in the press release about his departure which states, “The Corporation has been informed by Cyrus that they continue to support High Arctic and its Board of Directors in their efforts to maximize value for all shareholders through the contemplated reorganization.” Chairman Binnion states in the same release, “[Dan’s] departure provides the rest of the board the opportunity to independently contemplate imminent key decisions, in the interest of all shareholders”.

Let’s pause here to summarize. As of early May 2023, High Arctic was a cash rich energy services company with operations in PNG that looked set to inflect positively. With an enterprise value of $10-$20 million giving little credit for its Canadian assets and a PNG business that had earned more than $50 million in operating income in a single year at prior peak, the stock seemed undervalued. Instead of simply allowing the turn in PNG financial performance to play out in the public markets, the Board proposed to dividend out the bulk of its cash and privatize the PNG business through a rights offering. CFO Lance Mierendorf resigned a few weeks after the reorganization was announced (apologies to the reader, I failed to fit in that development earlier). Both representatives of Cyrus, the company’s 45% shareholder, left the Board by August and VN Capital, owning 5.6%, publicly requested the Board cancel plans for the PNG privatization in late August.

The Board and management never bothered to explain to shareholders why a private spinoff of the PNG assets, as opposed to a public spinoff or sale to a third-party, is the superior course of action. Given that some shareholders would not or could not participate in a privatization of the PNG business, it is natural to conclude that Cyrus and the Board favoured the structure as a way to increase their ownership ahead of an inflection in results.

Subsequent to VN Capital’s letter, the mess continues. In late September, the company announced that:

“The Corporation has received feedback from shareholders and is working with its advisors on the reorganization plan to incorporate key elements of the shareholder feedback. The High Arctic board has reserved its final decision to proceed with the reorganization until these matters and ongoing strategic review have been addressed to their satisfaction, requisite regulatory approvals have been received, and the materials are ready to present to shareholders.”

With the privatization plan now apparently canceled, VN Capital requested a special meeting in late-October to remove Chairman, Michael Binnion. The company then:

Suspended its dividend,

Restated its 2022 financial statements because of a very minor segmented disclosure issue,

Wrote down the value of its PNG assets by $20 million based on uncertainty around future drilling activity levels, and

Became more cautious on public calls about the potential for an uptick in its PNG business citing plans by the government to build roads to drill sites in the future.

The vote called by VN Capital to replace Binnion as Chairman is scheduled for January 10th. Cyrus will be the decisive vote, but they have said nothing publicly about their intentions. Absent any public comments from Cyrus, the fact pattern is suspicious and shareholders may conclude the worst about their intentions. The Board must explain, clearly and in public, why they decided to privatize the PNG business instead of pursuing a public spinoff, a sale to a third-party, or the status quo. In fact, one of the reasons provided by the Board for pursuing a separation of the PNG business in its circular for the upcoming meeting is, “enhanced potential for a future listing of the PNG business on an exchange in the Australasian region.”2 So why not just pursue a direct public spinoff or wait until such a spin is possible?

What are the benign explanations for such an unorthodox restructuring? Perhaps the Board became overly focused on tax efficiencies while forgetting that many shareholders not named Cyrus would want or need some liquidity? PNG is a difficult jurisdiction in which to operate. Perhaps the Board felt some of these challenges would be easier to manage out of the public eye?

At $1.15, the stock is obviously very cheap relative to assets and past earnings. Book value is close to $2 per share even following the recent PNG write-down. NWC per share is $1.19. High Arctic has a 42% stake in a Canadian snubbing business valued at $8 million, an additional $3.4 million promissory note owed from the snubbing business, a small Canadian rental business, four Alberta real estate properties, and $130 million of Canadian NOLs.

The potential upside from the PNG business is in doubt as some investors question whether the company’s two heli-portable rigs are in proper working condition. If roads are built to the wellsite, as management recently claimed is the government’s intention, the need for the company’s rigs may be eliminated entirely. However, should operating income return to even half of prior peak at $25-$30 million and assuming a very modest 3x multiple, the stock would be worth in excess of $2.30 per share, or twice the current share price.

Merry Christmas!

https://www.accesswire.com/778287/high-arctic-energy-services-inc-shareholder-urges-board-to-scrap-proposed-papua-new-guinea-business-spin-off

https://haes.ca/wp-content/uploads/2023/12/HAES-2023-Management-Info-Circular-Special-Meeting-FINAL51091353.1.pdf