Deciphering CI Financial

Deciphering CI Financial

Making Sense of an Oddly Messaged Transaction

CI Financial is not a rinky dink resource exploration company listed on the TSX Venture exchange. But for a couple days in mid-May, it acted like one. Sporting a $2.3 billion market cap, the stock jumped 50% at one point on May 11th, adding over $1 billion of value. By the close on May 12th, CI’s stock had retraced the entire move.

Prior to market open on May 11th, CI announced the sale of a 20% stake in its nascent US private wealth business for $1.35 billion (US$1 billion). This, according to the CI press release, implied a value for the US business alone of $6.7 billion or roughly three times that of CI’s market cap and modestly more than the company’s enterprise value. The majority of CI’s EBITDA is actually generated by its Canadian asset management business. That a division producing only a quarter of CI’s EBITDA could be worth more than the value ascribed by the market to the entire company seemed like very positive news. The type of news that would justify an additional billion dollars of equity value, or more.

The real terms of the investment in CI’s US wealth franchise are significantly different than presented by management in the press release and on the conference call held that morning. CI did not sell a 20% equity stake; it really sold a $1.35 billion preferred share with a 14% minimum coupon paid in kind. Investors are left wondering: why did management obfuscate the terms of this investment and what are the prospects for CI shares?

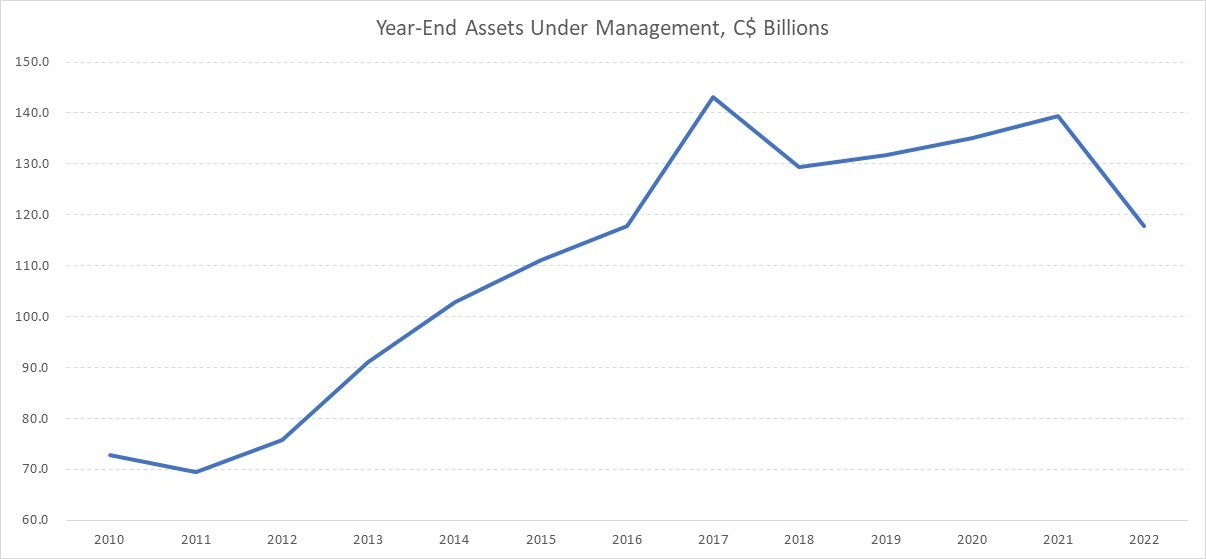

Rewind to 2019. CI Financial was, and still is, one of the largest independent asset managers in Canada with $129 billion of assets under management at the end of 2018. The stock was rangebound, drifting sideways for almost 15 years. CI’s assets under management plateaued as investors increasingly favoured low-cost passive options. That CI’s investment performance was lagging peers did not help. Regulators were requiring increased transparency in client disclosures which, along with competition from passive, was also hurting fees. Asset managers can be great businesses when things are going well – they are capital light with very high incremental margins – but challenged when trends reverse because of high decremental margins.

Generating good cash flow, but potentially in terminal decline given the industry and company-specific headwinds, CI increasingly felt like a melting ice cube. In September 2019, the CI Board took the bold step of hiring an outside CEO to reinvigorate the company, 38-year-old Kurt MacAlpine.

MacAlpine immediately began to transform CI. On his first public earnings call, only two months after joining the firm, MacAlpine announced that CI would be entering the US registered investment advisor (RIA) market. RIAs provide financial advice - covering areas including investments, estate, and tax - to high-net-worth individuals and generally charge a fee as a percentage of clients assets. On the decision to diversify into the RIA market, MacAlpine said:

“…RIAs are wealth management firms that uphold a fiduciary standard with their clients. They account for 23% of the US wealth management market today and are growing at a rate of 18% per year. The market is also highly fragmented, with 90% of all firms being independently owned. I believe we’re a natural owner of these businesses for a few reasons.

“In addition to having extensive experience operating wealth management businesses, we have a unique value proposition compared to others that are currently in the market. We have scale across many of the key functions; we can provide financial planning, asset allocation and investment management capabilities; we’re well-capitalized and offer a permanent capital solution for these owners. Our existing $47 billion wealth management businesses will also be a great source of cross-border referrals.”

RIAs are outgrowing the rest of the wealth management industry in-part because of an increased client preference for the alignment of a fiduciary standard. The focus on holistic wealth planning as opposed to just investment advice relative to traditional advisors also creates a deeper client relationship, tying the client to the firm, not just the advisor. This produces a more attractive margin profile at the RIAs. Margins in traditional wealth advisory businesses tend to be slim because the advisor owns the client relationship1. When advisors switch firms, 90% or more of clients typically follow. Returns in traditional advisory businesses tend not to be earned directly from the client relationship, but indirectly by selling house investment product through the advisor.

On that first earnings call in November 2019, MacAlpine disclosed that CI was not just planning to enter the US RIA market, but that it had already done so, signing letters of intent for two acquisitions. From there, CI proceeded at a brisk pace, spending approximately $2.5 billion in 2020 and 2021 acquiring additional RIAs. The US Wealth segment exited 2021 with $146 billion of AUM.

Investors and analysts were skeptical of CI’s diversification strategy. Was CI really the logical owner of these businesses? It did not help when Rudy Adolf, the CEO of Focus Financial, a larger RIA roll-up, took a thinly-veiled dig at CI on the company’s Q4 2020 earnings call: “…we have to be just very, very disciplined…last year, we called internally the year of the drunken sailors.” Despite repeated analyst inquiries, CI refused to disclose the multiples paid for its RIA purchases, citing competitive concerns.

CI was also less than fully transparent about the structure of its acquisitions. With selling shareholders key to the ongoing operations of the business, it is important to incentivize management to remain with the RIA and perform under new ownership. CI deferred some of the acquisition consideration and included payments that would be contingent on future performance, but these amounts seemed to pay out over shorter periods than those at Focus Financial. Selling shareholders also retained an equity stake in the overall US franchise, but this appeared to be monetizable in relatively short order2. In early 2023, these concerns manifested when the CEOs of Segall Bryant & Hamill and RegentAtlantic retired within two years and one year respectively of their acquisition by CI.

CI stock rallied sharply through much of 2021 but then rolled over in-line with the broader market sell-off later in the year. With the company’s Q1 results in May 2022, MacAlpine announced an intention to pursue an IPO of a minority stake in the US RIA business. He explained the IPO decision this way:

“We believe and are very confident and I think hopefully, investors see, based upon the quality of the business that we’ve assembled, the organic growth rates that we’ve achieved, the fee capture that we’re generating, we have an incredibly valued business, a valuable business that isn’t being valued by our shareholders as we’re currently constructed.

“So over a series of months, the Board was having conversations around how do we best unlock this value for our shareholders while maximizing all the strategic flexibility in keeping the great benefits associated with the business that we’ve built and will continue to build going forward.”

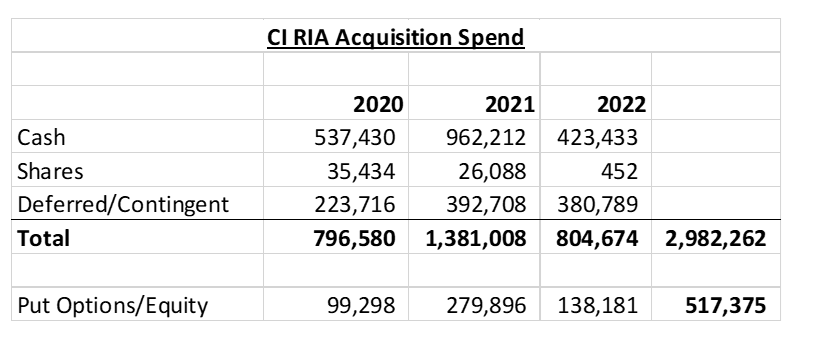

In other words, selling 20% in an IPO would illuminate for investors that they were underappreciating the RIA franchise. CI continued to acquire RIAs through the balance of 2022, spending about $900 million for the year, taking AUM up to $174 billion by year-end. Over the three years that CI spent aggressively on RIA acquisitions from 2020 to 2022, the company also repurchased 17% of its shares outstanding for $850 million. The torrid pace of capital deployment took gross leverage up to 4.2x adjusted EBITDA by the end of 2022 from 1.9x at the end of 2019.

With equity market conditions challenged in early 2023, CI could not execute the planned IPO. Instead, management went ahead with the preferred share sale to a group of investors including Bain, Ares, and the Abu Dhabi investment Authority. There was nothing in the May 11th press release about a guaranteed 14% minimum return, only that “each holder of preferred equity is entitled to receive a liquidation preference.” This was the second last line of the release. Similarly, on the public call following the deal announcement, MacAlpine almost seemed to go out of his way to avoid mentioning the 14% minimum return:

“So we set it up as preferred equity for two reasons. So the investors are buying into the subsidiary business of a public company where, by definition, they have limited rights. And not all the capital that we’ve received is permanent, which means some of them will need to return it to their ultimate investors at some point in the future. So we set it up this way to ensure that they have necessary liquidity for their shareholders in the future at a valuation that’s fair, recognizing the complexity of being inside of a public company as a minority subsidiary business.

“So in terms of the terms themselves, I mean, it was very attractive for us just given the quality of the business we’ve built plus the scarcity value, which allowed us to structure it in a very friendly way for our shareholders. So their equity votes in line with their ownership. They have one Board seat as part of our 6-person Board. In the event, and I think this is where you’re going, that we’re not public in 2030, they do have a liquidation preference to ensure that they have an ability to get their capital back and return to their shareholders at terms that are fair and reflective of the value of the business, whether we IPO or take a different route.”

And later:

Analyst: “So I think in the summary of the terms you suggested that you have the right to buy back the minority investment at the entry value plus a minimum return. What were you alluding to on the exit rates, does the group have the right to sell back that minority investment to you at the same entry value plus the minimum return? Is that what you’re alluding to?”

MacAlpine: “No. No. They have a right to pursue an exit. That could be via us going public, which is the intended path. As I mentioned, this is a pre-IPO stake. That’s the path that we intend to take. In the future, they have an opportunity to sell their stake, which we could be a buyer of that stake.”

No mention of a minimum guaranteed return. To discern the true parameters of the investment, analysts turned to the material change report filed on Sedar at 9:06 am on May 11th. Specifically, the sections on Conversion and Liquidation Events. For those that enjoy parsing legalese, the full text of those sections is below. In plain language, the $1.35 billion investment will pay out at a minimum of $2.0 billion if the US wealth business is monetized within three years and then accrete at 14% per year after that to $3.0 billion in year six. If the RIA business sells for $4 billion in 2026, CI will pocket $2.0 billion. If it sells for $3.4 billion in 2029, CI will only keep $400 million. Only in a scenario where the business is monetized at an equity valuation of $10 billion or more within three years would the preferred act like a 20% equity stake. I will leave it to the reader to assess whether a $10 billion valuation is realistic, equating to 36x 2022 adjusted EBITDA for the segment.

There is additional complexity. The US subsidiary will assume about $400 million of contingent consideration liabilities associated with RIA acquisitions previously completed. Selling RIA shareholders also appear to have a claim on about 20% of profits from the US subsidiary and this interest can be redeemed over the next 18-24 months in cash. At Q1 2023, CI valued this interest at C$794 million while the actual cash payout is likely to be closer to C$938 million3. Within a couple years, it appears the RIA business may distribute as much as $1.3 billion in additional cash.

Management says that as of Q1 2023, annualized adjusted EBITDA for the RIA business is $275 million. This excludes roughly $50 million of non-controlling interest related to the 20% claim held by selling shareholders. If we assume the RIA business generates an average of $175 million of free cash flow over the next two years, the business may still be left with as much as $950 million of debt or leverage in excess of 2.5x in late 2025. Also, investors must wonder whether RIA management will be properly motivated and aligned if their residual economic interests are fully monetized. Has CI appropriately structured these acquisitions to ensure continuity beyond the next couple years?

By 2025, assuming no additional RIA acquisitions, the subsidiary would have $950 million of debt, a $2 billion preferred liability and maybe something like $375 million of EBITDA (assumes 7% annual growth and the consolidation of the $50 million of EBITDA from the non-controlling interest). RIA roll-up Focus Financial was acquired by Clayton, Dubilier & Rice in February 2023 for about 11x EBITDA. If CI’s business commands the same multiple in two years, CI’s stake would be worth $1.2 billion. At 8x it would be worthless. That’s a lot of torque!

In practice, the US wealth business is likely to continue acquiring RIAs with debt which will increase leverage further. I find it highly improbable that CI will recover the approximately $3.2 billion that I estimate they spent on RIA acquisitions to-date4. The value of CI’s remaining ownership will likely not be crystallized for years; it could be worth zero or a couple billion. I suspect we’ll see oscillation in investor sentiment on this issue which could drive volatility in the stock given the market cap is only $2.4 billion.

The Canadian asset management business remains the core earnings driver for CI, producing $730 million of adjusted EBITDA in 2022. MacAlpine completed a significant restructuring program at the manager over the past few years, consolidating the fund families like Signature, Cambridge, and Harbour under one brand and one investment team. While this move reduced operating costs, the long-term impact to client and advisor relationships as well as investment performance remains to be seen.

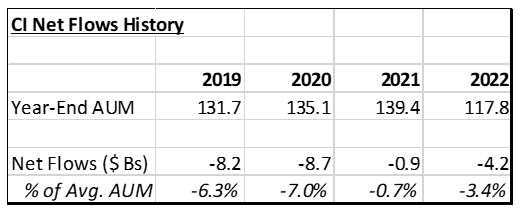

Net flows, while still challenged, improved in 2021 and 2022 on rebounding investment performance; CI improved from 37% of funds outperforming the peer average on a three-year basis in late-2020 to 72% outperforming by mid-2021. CI also experienced success with a high interest savings ETF given the more favourable rate environment. The ETF enjoyed billions in positive flows in 2022, sitting with $6.4 billion of assets as of April 2023. Unfortunately, it carries a paltry management fee of only 14 basis points.

With the shift to passive pressuring flows and fees, I think it is most appropriate to view CI’s asset management arm as a melting ice cube. EBITDA will likely remain under pressure and cash conversion will be adversely impacted by regular restructuring charges needed to right-size the expense base for reductions in asset levels5.

Asset management EBITDA in Q1 2023 annualized was $660 million. Assuming net flows of -4% annually, the average over the past four years, along with a low single digit headwind from fee compression, topline could be down mid-to-high single digits annually prior to market effects. On a highly fixed cost structure, this could pressure EBITDA by 10-15% per year without offsetting restructuring. In a base case with flat markets, I would assume 2023 EBITDA lands at $640 million for the segment and falls 10% annually with 2% of EBITDA spent on restructuring.

Rounding out CI’s divisions is a Canadian wealth advisory business. Generating only $54 million of adjusted EBITDA in 2022 it is more important as a contributor of flows to the asset management franchise than as a standalone profit engine (27% of CI’s AUM in the asset manager is gathered through its advisory business). If we use publicly-traded competitor Richardson Wealth to value the asset, currently trading at 5-6x EBITDA, CI’s business is worth $250-$300 million, though perhaps as much as twice that level to a strategic buyer.

Pro-forma for the $1.35 billion preferred transaction, CI will have net debt of approximately $2.9 billion. Excluding the RIA business, I estimate CI will generate about $700 million of EBITDA in 2023, putting leverage at 4.1x. However, CI’s go-forward debt structure is highly attractive. I expect CI will be able to discharge the remainder of the RIA acquisition liabilities not going with the subsidiary out of free cash flow in the next one or two quarters. This will leave three outstanding bond issues: $400 million December 2025s with a 7.0% coupon, $1.3 billion December 2030s with a 3.20% coupon currently trading at 75 cents, and $1.2 billion June 2051s (not a typo) with a 4.10% coupon currently trading at 58 cents. There are no material covenants on these bonds.

MacAlpine says the go-forward plan is to effectively privatize the Canadian business through share buybacks. With the favourable maturity profile and cost of debt, CI should have significant free cash flow available to repurchase shares. Assuming the company maintains its current dividend policy, I estimate CI could retire up to 20% of shares outstanding over the next two years. The free cash flow yield is about 15% assuming no value to CI for the RIA business.

CI’s share price will be driven by AUM and EBITDA trends in the Canadian asset management business plus investor sentiment regarding the ultimate realizable value of the RIA stake. A further monetization event within the US wealth business appears unlikely in the near-term and so investors will be left to speculate about the value which could plausibly range between zero and $2 billion or more. The RIA business is opaque. Did CI buy quality assets? Did they structure the purchases appropriately to retain staff and clients over-time? The business was cobbled together so rapidly and disclosure is so limited that it is difficult to say.

The asset manager is likely a melting ice cube but should still generate good cash flow for many years. CI’s go-forward debt structure is favourable. The only value-added capital allocation decision that MacAlpine seems to have made during his tenure was to issue the 2030 and 2051 bonds. At market prices, these bonds are now worth $825 million less than par.

The bull case for CI is strong markets and minimal net redemptions driving flattish EBITDA in asset management. With a robust market backdrop, investors might attribute $1 billion or more of value to CI’s RIA stake. CI could be generating $400 million of free cash flow to equity in this scenario with a $2.4 billion market cap. Perhaps investors would be willing to deduct the $1 billion assumed RIA valuation from the market cap, leaving an implied 29% free cash flow yield on the remaining equity. The stock could double or triple in this scenario.

The bear case would be weak markets and negative flows driving EBITDA down 20% or more. Investors may write-off the RIA stake. This would leave CI with a 10% declining free cash flow yield, and significant leverage, though long-dated. Even then, to get to a 15% free cash flow yield in this scenario, the stock would only fall by 25%.

CI is not a wonderful business, but the stock feels like a buy to me. I don’t own any at the time of writing.

Though investors now generally understand the structure of the preferred investment in the RIA business announced on May 11th, they are left wondering one thing – why? Why would CI management obscure the truth about the terms of the preferred shares to the point where the market added and then subtracted $1 billion of market cap over two days?

My guess is that it was, perhaps ironically, an attempt to save face. It’s hard to bet the company on a new strategic direction, deploy billions in capital, and then almost immediately admit the whole thing was a mistake, especially if you were paid $10 million in 2021 for your efforts6. Even though the preferred investment in some ways crystallized the value destruction, it was still the right move because it deleveraged an increasingly strained balance sheet. I’m betting that this massive communication misfire is a function of management ego rather than a deliberate attempt to mislead. If only CI had skipped the whole RIA misadventure and done something else with the capital, the stock would be higher today.

For example, CI’s Canadian advisory business earned a 7% adjusted EBITDA margin in 2022 as compared to more than 30% in the RIA segment.

See for example this disclosure from Focus Financial. Nothing comparable is available from CI.

This amount includes an incremental $144 million of unrecognized compensation expense that will accrue to the unit liability through December 2024.

In an earlier version of this post, I incorrectly wrote that CI spent $3.5 billion on the RIA acquisitions. In fact, CI paid approximately $3.0 billion through a combination of cash, shares, and deferred/contingent consideration. The additional $500 million is the value of the residual economic interests retained by selling shareholders. Since I have not included the minority interest EBITDA in my analysis, it is incorrect to include the outstanding liability for those residual interests.

CI recorded about $175 million of change in the fair value of contingent consideration in 2021 and 2022 and a corporate total of $160 million of transaction, integration, restructuring, and legal charges from 2020 to 2022 (only some of which relates to the RIA business). So the true all-in cost of the RIA acquisitions is probably something like $3.2 - $3.3 billion.

With the current EBITDA run-rate for the segment of $275 million, the effective purchase price is 11-12x on current EBITDA (not quite “drunken sailor” territory). I suspect the multiple paid on year one EBITDA was higher, but that it has come down on good earnings growth. Note: the $275 million of run-rate EBITDA is a management-disclosed figure. Reported EBITDA for the segment in 2022 was $220 million, but this does not include the full benefit of acquisitions and organic growth completed during the year.

Restructuring charges have ranged from 3.5% to 7% of adjusted EBITDA over the past four years, though this included transaction costs associated with the RIA build-out.

MacAlpine was paid $10.6 million in 2021, falling to $7.3 million in 2022.