GMP Capital: Value is in the Eye of the (Strategic) Beholder

GMP Capital: Value is in the Eye of the (Strategic) Beholder

GMP Capital is in the midst of significant change. After shedding its core capital markets business in a sale to Stifel last year, the company is now transforming into a pure-play financial advisory business by consolidating its 34% ownership in Richardson GMP. TD Bank was rumoured to have bid for Richardson GMP at a $760 million enterprise value in 2016. At that valuation, GMP Capital’s stake in the wealth manager would be worth $3 per share – twice the current GMP share price of $1.50 – plus GMP has an additional $1 per share of net working capital. Does the rumoured TD offer from 2016 present a fair picture of the value of the wealth manager, representing, as it did at the time, an astounding 36x EBITDA? Are the proposed terms of the consolidation of Richardson GMP fair to GMP shareholders? And what can we learn about the wealth management business in Canada by studying Richardson GMP?

Spoiler alert: I don’t have a strong view on the attractiveness of GMP stock.

Following the capital markets sale, GMP is essentially a publicly traded holding company. It's two major assets are $123 million of net working capital and its 34% stake in Richardson GMP (I will abbreviate as RGMP, which, keep in mind is not the same as the publicly traded parent, GMP). RGMP’s 165 advisory teams provide financial advice and planning to high net worth individuals, overseeing $28.2 billion of assets as of the end of Q2. RGMP was formed in 2009 through the merger of the financial advice businesses of GMP and Richardson Financial and augmented with the 2013 acquisition of Macquarie Private Wealth. The two-thirds of RGMP not owned by GMP is split roughly evenly between the Richardson family (who also control about one quarter of GMP stock) and RGMP advisors and management.

The difficulty with the financial advisory business in Canada is that the key asset – the relationship with the end customer – is owned by the advisor. The relationship is largely a personal one, independent of the advisor’s affiliation. This is especially true for independent firms like RGMP where there is no broader institutional relationship, a mortgage or savings account, as might exist at the wealth management arms of the big banks. And so the advisor is well-positioned to command the vast majority of the economics; if the money is better elsewhere, the advisor can simply pack up and move.

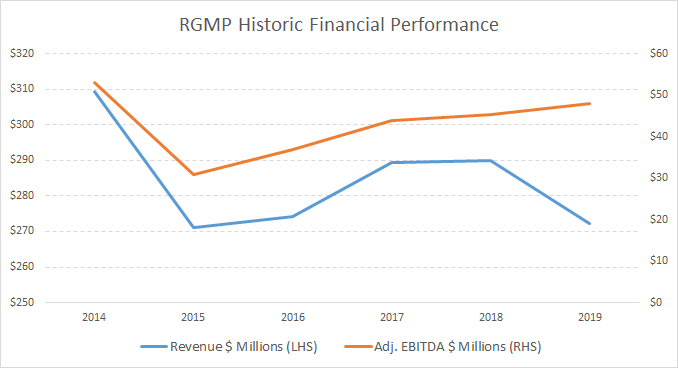

Financial performance at RGMP has been underwhelming over the past five years. Revenue has been stagnant in the $275-$300 million range and assets have bounced around from $25-$30 billion. Adjusted EBITDA margin has improved somewhat over the period from the low-teens in 2015 to the 15-18% range more recently. When assessing RGMP’s performance, note that adjusted EBITDA excludes stock-based compensation (adds about 100 bps to margins) and amortization of transition loans (adds 300-500 bps). The transition loans are used as a recruitment tool and forgiven once the advisor has been with the firm for a set period. According to management, these are really more like one-time acquisition payments to lure advisors; the amortization should be excluded from adjusted earnings. But asset levels and the advisor count have not grown in years. These seem more like operating expenses to me.

RGMP has often been rumoured as an M&A target in recent years. TD was thought to have bid $600 million for the equity of the business in late-2016 ($760 million EV) before the deal collapsed. The Financial Post at the time speculated the acquisition fell apart because of a lengthy negotiation process, public leaks, and poor communication from RGMP management to advisors. Concerns from TD about advisor retention in the hands of a bank may have also been a factor. As an independent firm, RGMP advisors can offer unconflicted advice. In the hands of TD, or any other bank, this independence would be compromised. In fact, the main synergy to an acquirer would be the ability to sell its own investment and banking products through the RGMP advisors.

To that point, we can use CI Financial and its ownership of advisors Assante and Stonegate as an illustration of the potential synergies from bank control of RGMP. Assante and Stonegate have about $50 billion in assets under administration and are break-even on a pre-tax basis. 60% of the assets in the advisory business are invested in CI funds. The asset management segment has a pre-tax margin of about 42%. So, even though the advisory business is break-even, it contributes about $30 billion of assets to the mutual fund business, which, at a management fee of about 1.4% and 42% margin drives $175 million of pre-tax income.

Let’s assume a bank could achieve 50% penetration of proprietary product at RGMP. This would drive $14 billion of additional assets under management or $90 million of incremental pre-tax income with similar management fees and contribution margins to CI. Even assuming RGMP generates zero profitability on a standalone, pre-synergy basis, TD would earn a 12% pre-tax return on the $760 million offer price. Not too shabby!

For some context, a purchase of the business for $760 million would represent about $4.6 million per advisory team. One would suspect that TD should be able to “poach” at least some of the advisors from RGMP for substantially less, casting doubt on the potential for an offer at that valuation to ever materialize. Further, a $760 million purchase price would be 17x adjusted EBITDA over the most recent 12 months or 24x unadjusted EBITDA – quite rich!

On August 13th of this year, GMP announced a definitive agreement to consolidate ownership of Richardson GMP. While the value received when a company does an acquisition is not always clear at the time the deal is announced, the value paid, in terms of cash or shares, is usually fairly apparent. Not so for the RGMP transaction! We have to work a little to make sense of the proposal.

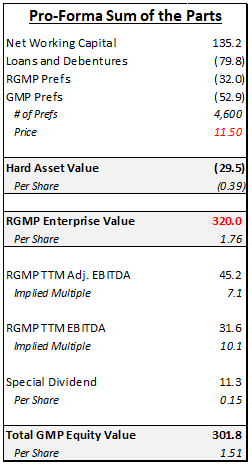

Let’s start with the favourite analytical tool of the investor about to make a money-losing decision – a sum of the parts analysis for GMP as it exists today. The two key assumptions are highlighted in red – the enterprise value of RGMP and the value of the GMP preferred shares.

Under the terms of the August agreement – slightly improved from a preliminary February proposal - GMP would issue 106.9 million shares to Richardson Financial and the RGMP advisors (as compared with 75.4 million GMP shares currently outstanding). RGMP advisors would also receive $36 million of cash retention awards and current GMP shareholders will receive a $0.15 per share special dividend prior to close.

There is no perfect way to turn the proposed terms of the deal into a single number which can be assessed for fairness. But here’s my attempt. Effectively, GMP Capital is a cash-rich holding company that will contribute its assets and liabilities in exchange for a greater equity stake in RGMP. The value of the hard assets and liabilities – cash, debt, and prefs – is known. The value of RGMP is not.

Under the August proposal, existing GMP shareholders, including the Richardsons, will go from owning 34.4% of RGMP to 41.4%, picking up an additional 7% equity. In exchange, valuing the outstanding GMP preferred shares at $11.50 per share, in-line with recent trading prices, GMP Capital will contribute about $77 million of hard net asset value. This implies an equity value for RGMP of close to $1.1 billion – clearly too high!

Let’s not forget that on a standalone basis, GMP Capital also has corporate overhead costs, running at a bit over $2 million in the latest quarter. An alternative to pursuing a consolidation transaction could be to wind-down GMP Capital and distribute all the assets to shareholders. In such a scenario, assume we incur 2x the annual overhead costs as wind-down charges. This would drive the implied valuation of RGMP to a more reasonable, though still elevated, $850 million. It could also be argued that the preferred shares could not be retired at market, but some premium would have to be paid. At $15 for the prefs and $18 million in liquidation costs, the implied RGMP value is closer to $550 million; still on the high-side. Perhaps GMP shareholders should hold-out for another $0.10-$0.20 per share ($350-$450 million valuation implied for RGMP).

The table below shows my estimate for the additional dividend (beyond the $0.15 already promised) required to make existing GMP shareholders indifferent between a liquidation of GMP Capital and the consolidation of RGMP.

Let’s assume the RGMP consolidation is approved by shareholders as proposed. Are GMP shares attractive? Given the need to retain advisors, I worry that the free cash flow generation available to shareholders will be modest over-time, certainly well-below the adjusted EBITDA figure. The proposed transaction terms underscore the concern around advisor retention. 90% of the new GMP shares issued to the advisors will be locked-up and released in equal installments annually over three years. Advisors will also receive $36 million of retention awards, to vest over an undisclosed period. What will happen in three years when the $36 million advisor retention award is a distant memory and the lock-up period on the shares expires? My guess is more retention payments and more share awards.

However, the strategic value of the RGMP business is potentially significant. At the rumoured enterprise value on the TD bid from 2016 of $760 million, GMP shares could be worth close to $4 or 175% more than the current share price. TD, or another bank, might be perfectly content to own a break-even advisory business if they can sell more of their in-house investment funds through the channel.

Resorting to our favourite money-losing analytical tool again, at the current share price of $1.50, the stock is implying an enterprise value of about $320 million for RGMP or 7.1x trailing adjusted EBITDA.

Through all the complexity, the proposed terms of the RGMP consolidation appear somewhat unfair to GMP; shareholders feeling greedy should hold out for another $0.10-$0.20 per share. On my math, the current share price is implying a value for RGMP in the low-$300 million range while the consolidation is being proposed at a valuation of mid-$500 million. This is quite a gap.

RGMP will be the key driver of the stock moving forward. On a standalone basis, RGMP is not that profitable and will be perpetually fighting to prevent the key asset – advisors – from walking out the door. The retention bonuses and share lock-up will likely support a holiday on this issue for a few years, giving the company some time to sort out its strategy, but inevitably retention issues will resurface. On a standalone basis, given these concerns, I struggle to wrap my head around an appropriate valuation for RGMP. However, synergies in the hands of a strategic acquirer could support a price tag well in excess of the current $320 million implied by the market.

And now for the anti-climactic conclusion, facilitated by two sum of the parts analyses – I don’t have a strong opinion on the stock.

Left out of this discussion, but perhaps worthy of closer examination, is the question of why so much synergy can be generated by an advice business in the hands of a manufacturer of investment products. After all, shouldn’t the advice be independent of the advisor’s affiliation, focused solely on the needs of the client?

Disclosure: the author has no position in GMP Capital.